This Ultimate Growth Stock Is Down 66%: Time to Buy the Dip?

There is perhaps nothing more powerful than an expanding consumer packaged food brand with a huge target audience. Brands like Coca-Cola , PepsiCo (NASDAQ: PEP) , Hershey , and Gatorade are just some of the examples out there. Once a new consumer brand takes hold and has national (or even international) distribution, a long growth runway suddenly emerges. Even better is if the product category itself is getting added consumer attention.

Such is the case with Celsius (NASDAQ: CELH) . The energy drink producer has been growing like gangbusters over the past decade, and that helped boost its stock price over that decade by more than 40,000% at one point earlier this year. Unfortunately, the fizz in this drink maker is starting to flatten.

Celsius stock is trading down nearly 67% from all-time highs set in early June as it works through a new distribution relationship with PepsiCo and manages concerns that the energy drink category is slowing. Investors turned pessimistic about its future growth prospects over news that its revenue growth rapidly slowed down in recent quarters.

With shares now trading much cheaper than at the start of the year, let's see if now is a good time to take the leap and buy some Celsius stock for your portfolio.

Celsius: Reinventing energy drinks

Celsius entered the energy drink market by targeting consumers interested in eating (and drinking) healthier and in search of sugar-free and vitamin-infused energy drinks. This is a different brand narrative than what Monster Beverage or Red Bull convey to their potential customers. Going down this marketing path, Celsius built up a huge presence in the fitness industry and with female consumers.

Over the last five years, Celsius' grew its revenue by over 2,000% and it is now the third-leading brand in the energy drink category in the U.S. with a 5.9% market share (as of 2023). Revenue was $1.49 billion over the last 12 months. The vast majority of sales still come from North America.

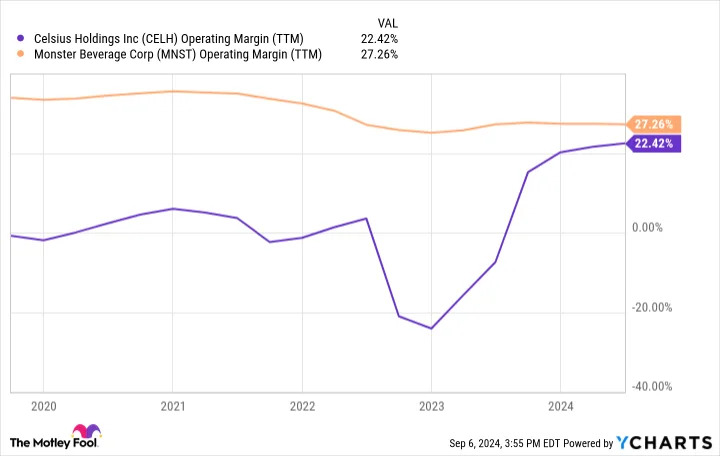

Growing scale has also led to growing profitability for Celsius. For years, Celsius either operated at a loss or close to breaking even due to its preference for reinvesting cash flow for future growth. Now, the company is reaching a large enough scale that the underlying unit economics of the business are shining through to the bottom line. Operating earnings were $334 million over the past 12 months, or a 22.5% margin. Monster Beverage -- its closest competitor -- has a 27% profit margin.

Pepsi pressure, slowing category growth

A few years ago, Celsius signed a big deal with PepsiCo to get Celsius on its distribution network. This enabled Celsius to obtain better shelf space in convenience and grocery stores, which is huge for consumer food and drink brands. This distribution change helped Celsius boost its growth rate immensely. In the second quarter of 2023, for example, revenue grew by over 100% year over year.

In the same period this year, revenue growth slowed to just 23%. What Celsius has told us now is that it oversold inventory to PepsiCo at the start of the distribution deal, which made revenue growth look better than it actually was. Now, we are seeing the opposite effect as PepsiCo works to normalize its inventory with the brand. To be clear, 23% growth is still impressive, especially when you consider the distribution headwind. There are no concerns that Celsius is losing its brand status in the U.S.

Another headwind is the overall energy drink category growth. Celsius management told investors at a recent investment conference that some energy drink players are seeing negative volumes as the whole category goes through a rough patch in 2024. It is unclear what is causing this slowdown, but over the long haul, energy drinks have taken a lot of share from traditional beverages such as coffee, tea, and soda. If I had to bet, I think this trend will continue -- especially with sugar-free energy drinks -- over the next few decades as well. This bodes well for Celsius.

The stock looks cheap

At a share price of $32, Celsius stock has a market cap of $7.5 billion. This is around 22 times its trailing operating earnings. While there are concerns about short-term growth for Celsius due to the category slowdown in 2024 and the PepsiCo distribution overhang, I think the stock looks cheap at 22 times earnings.

Long-term investors should have confidence in a few things. First, Celsius is still taking market share in the energy drink category. Second, energy drinks have shown the ability to raise prices without impacting demand. Third, the overall energy drink category has grown for many decades since the rise of Red Bull and Monster.

Take all three of these factors together and I think Celsius can post double-digit revenue growth for many years into the future. If that happens, investors who bought at today's prices will be pleased looking back five and 10 years from now.

Before you buy stock in Celsius, consider this: