Super Micro Shares Sink Despite Revenue Surge and Stock Split. Should Investors Buy the Stock on the Dip?

Following its fiscal fourth-quarter earnings report , shares of Super Micro Computer (NASDAQ: SMCI) sank 20% in the next trading session, even though the server solutions company announced a stock split and issued strong revenue guidance. Despite the pullback, the stock is still up about 70% on the year.

Let's take a closer look at the company's quarterly results, why it sold off, and whether investors should look to buy the dip.

Strong sales and guidance, but margin worries

For its fiscal fourth quarter, Super Micro saw its revenue surge 143% to $5.31 billion, which was pretty much in line with what analysts had expected. However, its earnings per share (EPS) of $6.25 fell well short of expectations of $8.07 due to gross margin pressure the company experienced in the quarter.

Gross margin , which measure the difference between what a company sells its products or services for versus how much it costs to provide those products or services, fell to 11.3% from 17% a year ago and 15.5% last quarter. The lower margins stemmed from product mix, lowered pricing to win new designs, and higher costs associated with ramping up its direct liquid cooled (DLC) rack scale AI GPU clusters. The company expects gross margins to gradually increase throughout its fiscal 2025 and eventually return to its targeted range of 14% to 17%.

The company credited its strong growth to its next-generation air-cooled and DLC rack scale AI GPU platforms. Servers generate a lot of heat, and these systems help keep them cool to stop them from failing while also reducing energy costs. Super Micro has seen a lot of demand for its DLC systems as companies build out their data center capabilities to run artificial intelligence (AI) applications. It noted that it has an over 70% market share in the DLC space.

Despite its tremendous growth, Super Micro said growth could have been even greater if not for a DLC liquid cooling component shortage. It estimated that about $800 million of revenue fell into July after its fiscal fourth quarter was over, due to the component shortage.

Looking ahead, Super Micro forecasts that full-year fiscal revenue will be between $26 billion to $30 billion. That would be a 100% revenue increase at the high end of its forecast after it generated $14.9 billion in revenue this past fiscal year.

For its fiscal first quarter, it is forecasting sales of $6 billion to $7 billion, with adjusted EPS of $6.69 to $8.27. The $7.48 midpoint of the range was below the $7.58 analyst consensus.

The company also announced a 10-for-1 stock split. While stock splits do not change the fundamentals of a company, the lower share price can attract more retail investors to a stock.

Should investors buy the dip?

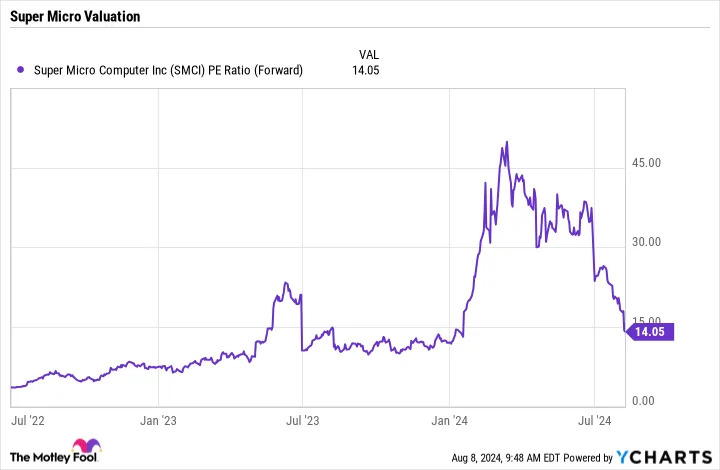

From a valuation perspective, Super Micro only trades at a forward price-to-earnings (P/E) ratio of 14 based on fiscal 2025 analyst estimates. Given its revenue growth, which is expected to about double next year, that is pretty attractive. That said, it is in a low-margin business, so it shouldn't command the multiple of a chip company like Nvidia or a software company like Microsoft either.

The company is currently seeing tremendous growth as it benefits from the AI infrastructure and data center buildout, but it also has to be somewhat concerning to see its gross margins so weak with demand for its products so high. That's not an indication of a business that has a wide moat or pricing power.

Given that fact, even after the recent sell-off, I'd probably wait on the sidelines a bit longer with Super Micro at the moment.

Before you buy stock in Super Micro Computer, consider this: